IBM as of today: Understanding the Company Before Its Competitors

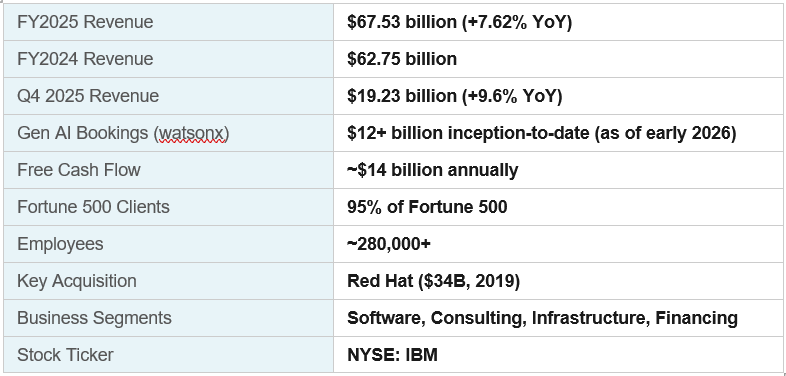

Before evaluating IBM’s competitors, it is essential to understand what IBM actually is as of today— because the company has changed dramatically from the hardware giant it once was. IBM (International Business Machines Corporation), headquartered in Armonk, New York, is now primarily a software and consulting company focused on hybrid cloud infrastructure and enterprise artificial intelligence. Its $67.5 billion in 2025 revenue is generated predominantly through two segments: Software (including Red Hat, IBM Cloud, watsonx AI, and automation tools) and Consulting (technology and business transformation services for large enterprises).

IBM serves 95% of the Fortune 500 and operates in more than 175 countries. Its generative AI platform watsonx, launched in 2023, has accumulated over $12 billion in bookings inception-to-date through early 2026 — a figure that has surprised many analysts who had written off IBM’s AI relevance. The 2019 acquisition of Red Hat for $34 billion remains the transformational move that repositioned IBM as the leading provider of open-source hybrid cloud solutions, with Red Hat OpenShift as the preferred enterprise Kubernetes platform globally.

IBM competes across three distinct battlegrounds: cloud infrastructure (vs. AWS, Azure, Google Cloud), enterprise software (vs. Oracle, SAP, Salesforce), and IT consulting and services (vs. Accenture, Infosys, TCS). Understanding this multi-front competitive landscape is essential for businesses evaluating IBM versus its alternatives — the right choice depends entirely on which battlefield matters most to your organisation.

IBM’s Competitive Landscape: Three Battlegrounds

IBM’s competitors can be organised into three categories, reflecting where IBM chooses to compete — and where it chooses to cede ground. In cloud infrastructure, IBM competes selectively, focusing on hybrid and private cloud rather than chasing AWS or Azure for public cloud market share. In enterprise software, IBM’s watsonx, automation, and middleware products compete with Oracle, SAP, and Salesforce. In IT consulting and managed services, IBM Consulting directly competes with Accenture, Infosys, TCS, and Capgemini for large enterprise transformation contracts.

What follows is an in-depth analysis of IBM’s ten most significant competitors in 2025, covering their revenue scale, market positioning, the specific areas where they challenge IBM, and critically — who should choose them over IBM, and why.

1. Microsoft Azure

The enterprise hybrid cloud leader with unmatched Microsoft ecosystem integration

| Azure Cloud Growth (FY2025)

40%+ YoY |

Global Cloud Share (Q3 2025)

20% |

| Azure Annual Revenue Est.

$80B+ (FY2025) |

Parent Revenue (FY2025)

~$280B (Microsoft) |

Microsoft Azure is IBM’s most comprehensive competitor across all three of its battlegrounds — cloud infrastructure, enterprise software, and AI consulting. In cloud infrastructure, Azure holds a steady 20% global market share (Q3 2025) and is growing at over 40% year-on-year — significantly faster than IBM’s cloud growth rate. In enterprise software, Microsoft 365 Copilot (AI integrated into Word, Excel, Teams, and Outlook) competes directly with IBM’s watsonx AI platform for enterprise AI mindshare and budget. In consulting, Microsoft’s partner ecosystem includes every major systems integrator, while its own professional services team competes with IBM Consulting on digital transformation engagements.

Azure’s primary competitive advantage over IBM is its breadth of integration. For any organisation already running Windows Server, Microsoft 365, or Dynamics 365, Azure is the path of least resistance to the cloud. Azure Active Directory (now Entra ID) provides identity management that ties the entire Microsoft ecosystem together — a lock-in that IBM’s open-source, vendor-neutral positioning explicitly tries to counter.

Where Azure Beats IBM

- Depth of Microsoft product integration (Office, Teams, Dynamics, GitHub, LinkedIn)

- Azure OpenAI Service — exclusive partnership with OpenAI gives Azure first-mover advantage in enterprise GPT-4 deployments

- Azure Arc for hybrid cloud extends Azure management to on-premises and multi-cloud environments

- GitHub Copilot dominates AI-assisted developer tooling — a space IBM’s watsonx Code Assistant competes in

Where IBM Beats Azure

- IBM’s open-source hybrid cloud (Red Hat OpenShift) avoids vendor lock-in concerns that Azure raises

- IBM Consulting’s industry-specific depth in financial services, healthcare, and government exceeds Microsoft’s

- IBM’s mainframe and legacy system expertise is unmatched — critical for banks and insurers with decades-old infrastructure

- Quantum computing: IBM Quantum leads Azure Quantum in hardware maturity and accessible qubits

2. Amazon Web Services (AWS)

The world’s largest cloud platform — IBM’s biggest cloud infrastructure rival

| Cloud Market Share (Q3 2025)

29% (#1 globally) |

AWS Revenue (2025 est.)

$115B+ |

| YoY Growth

~17% |

Data Centres

30+ regions worldwide |

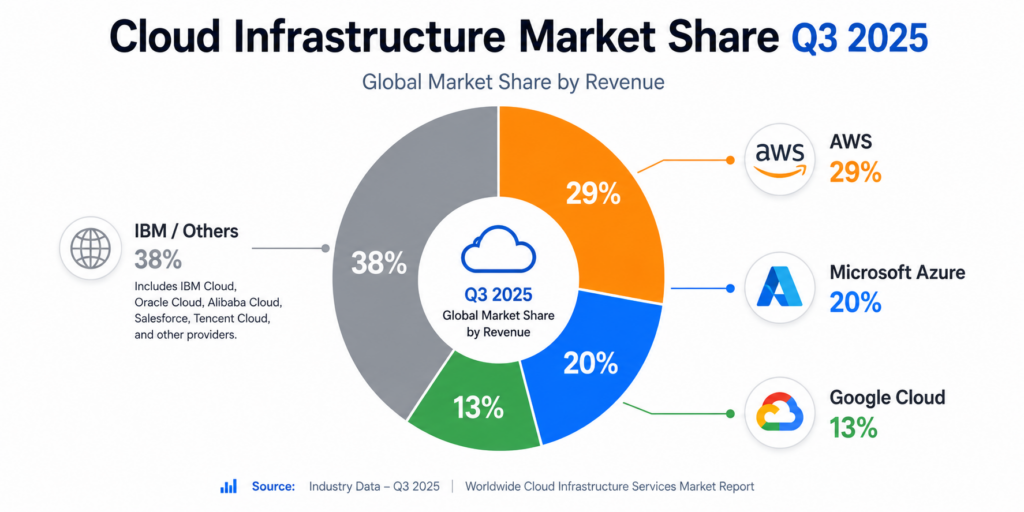

Amazon Web Services is the undisputed leader in public cloud infrastructure with 29% global market share — more than IBM’s cloud business by an enormous margin. AWS’s 200+ cloud services across compute, storage, databases, networking, machine learning, and IoT give it a breadth that IBM Cloud cannot match. For organisations building cloud-native applications from scratch, AWS is typically the default choice, offering the most extensive service catalogue, the largest developer community, and the deepest ecosystem of third-party integrations.

The critical distinction between AWS and IBM is strategic positioning. AWS is a public cloud-first platform optimised for developer agility and cloud-native workloads. IBM’s hybrid cloud strategy, built around Red Hat OpenShift, explicitly targets the opposite end of the spectrum: enterprises with complex legacy systems that need to run workloads across on-premises data centres, private clouds, and multiple public clouds simultaneously. IBM’s argument is that 80% of enterprise workloads have not yet moved to the public cloud, and that the reasons they have not — regulatory compliance, data sovereignty, latency, integration complexity — are exactly the problems IBM’s hybrid cloud platform is designed to solve.

Where AWS Beats IBM

- Largest cloud service catalogue (200+ services) and deepest technical feature set

- Amazon Bedrock provides a multi-model AI platform (Claude, Llama, Titan) rivalling IBM watsonx

- Best-in-class managed services for databases (Aurora, DynamoDB), containers (EKS), and serverless (Lambda)

- AWS Marketplace: 10,000+ third-party software listings — unmatched ecosystem

Where IBM Beats AWS

- Red Hat OpenShift is the #1 enterprise Kubernetes platform — runs on AWS, Azure, GCP, and on-premises simultaneously

- IBM’s consulting arm provides end-to-end implementation services that AWS Professional Services cannot match in scale or industry depth

- IBM’s Z mainframe systems handle transaction volumes that cloud-native alternatives cannot replicate cost-effectively

- Enterprise AI governance and explainability through watsonx.governance — critical for regulated industries

3. Google Cloud Platform (GCP)

The fastest-growing major cloud provider — leading in AI/ML infrastructure

| Cloud Market Share (Q3 2025)

13% (record high) |

GCP Revenue (2025 est.)

$50B+ |

| YoY Growth

~30%+ |

Key Strength

AI/ML & data analytics |

Google Cloud has reached a 13% global cloud market share — its highest ever — driven by its superior AI and data analytics capabilities. Where IBM competes on hybrid cloud and enterprise services, Google Cloud’s differentiator is its foundation in Alphabet’s AI research (Google DeepMind’s Gemini models, TPU hardware) and its world-class data infrastructure (BigQuery, Vertex AI). For data-intensive, AI-native workloads, Google Cloud is increasingly the preferred choice — particularly for organisations in media, retail, and consumer internet.

Google Cloud and IBM compete most directly in AI. IBM’s watsonx platform (built for enterprise AI governance, compliance, and hybrid deployment) and Google’s Vertex AI (built for scale, speed, and cutting-edge model access) represent different philosophies: IBM prioritises auditability and control; Google prioritises model capability and data scale. For enterprises in regulated industries (banking, insurance, healthcare) where AI decisions must be explainable and auditable, IBM’s approach resonates more strongly.

Where GCP Beats IBM

- Gemini 1.5 Pro and Vertex AI offer frontier model capabilities that IBM watsonx’s current model lineup cannot match

- BigQuery is the industry-standard serverless data warehouse — IBM’s Db2 Warehouse is a distant alternative

- Google’s TPU infrastructure provides unmatched performance for large-scale AI model training

- Best-in-class Google Workspace integration for productivity-layer AI features

Where IBM Beats GCP

- Enterprise consulting depth: IBM Consulting’s 160,000+ consultants dwarf Google Cloud’s professional services team

- Mainframe and hybrid IT expertise is entirely absent from Google Cloud’s portfolio

- IBM’s regulatory compliance coverage (FedRAMP High, DORA, financial services regulations) is broader and deeper

- IBM’s open-source philosophy via Red Hat aligns better with enterprises wary of Google’s data practices

4. Accenture

IBM Consulting’s most direct rival — larger, faster-growing, and vendor-neutral

| FY2025 Revenue

$70.72 billion |

Employees

~750,000+ |

| AI Revenue (2025)

$3B+ in GenAI new bookings |

Key Advantage

Vendor-neutral consulting |

Accenture is IBM Consulting’s most formidable and direct competitor, generating $70.72 billion in FY2025 revenue — making it larger than IBM overall when comparing pure consulting and technology services. Accenture’s 750,000+ employees give it a delivery scale that IBM Consulting (approximately 160,000 consultants) cannot match. The fundamental competitive distinction is this: IBM Consulting sells IBM technology; Accenture sells technology-agnostic transformation. This vendor neutrality is a significant advantage in large enterprise deals where procurement teams are wary of a consultant recommending their own products.

Accenture has invested aggressively in generative AI, accumulating $3 billion+ in new GenAI bookings in 2025 and retraining large portions of its workforce on AI implementation capabilities. Its AI refinery model — which helps enterprises move from AI experimentation to scaled AI deployment — directly competes with IBM’s watsonx implementation services. For enterprises looking for a pure consulting partner unconstrained by product allegiances, Accenture is typically the preferred alternative to IBM Consulting.

Where Accenture Beats IBM

- True vendor neutrality — no conflict of interest from recommending IBM products

- Greater delivery scale with 750,000+ employees across 120+ countries

- Stronger presence in digital transformation for consumer industries (retail, media, CPG)

- Accenture Song (marketing services) and Accenture Song Studios extend capabilities IBM Consulting lacks

Where IBM Beats Accenture

- IBM owns the technology stack — watsonx, Red Hat, Z mainframes — giving it unique IP that Accenture must source from third parties

- IBM’s mainframe expertise is irreplaceable for banks and insurers running mission-critical Z-series systems

- IBM Research (with 3,000+ researchers) provides a scientific depth Accenture cannot replicate

- IBM Quantum is the world’s most accessible quantum computing platform — a decade ahead of consulting firms

5. Oracle

The database king pivoting to cloud — IBM’s most direct enterprise software rival

| FY2025 Revenue

$61.01 billion |

Cloud Revenue Growth

~25% YoY |

| Database Market Share

~30%+ (global) |

Key Strength

Enterprise database & ERP |

Oracle is IBM’s closest competitor in enterprise software and database management. With FY2025 revenue of $61.01 billion and a pivotal cloud transformation underway, Oracle Cloud Infrastructure (OCI) has emerged as a credible alternative to both AWS and IBM Cloud, particularly for enterprises running Oracle databases and ERP systems. Oracle’s Autonomous Database — which uses machine learning to self-tune, self-secure, and self-repair — directly challenges IBM’s Db2 and IBM Cloud databases.

The competitive dynamic between IBM and Oracle is particularly intense in the financial services sector, where both companies have deep, decade-long relationships with the world’s largest banks. Oracle’s FLEXCUBE banking software competes with IBM’s banking solutions. Oracle’s Fusion ERP competes with IBM’s Maximo and enterprise automation platforms. The key differentiator: Oracle’s cloud strategy is built around its own database and application suite (enterprises move to OCI to run Oracle software better), while IBM’s hybrid cloud strategy is built around open standards and Red Hat (enterprises use IBM to run workloads from any vendor).

Where Oracle Beats IBM

- Oracle Database is the most widely deployed enterprise database — its cloud migration path is more natural for Oracle-heavy organisations

- Oracle Fusion ERP is a direct, more integrated alternative to IBM’s enterprise automation and ERP integration tools

- OCI’s bare metal and Exadata cloud infrastructure offers superior database performance at competitive pricing

- Oracle’s NetSuite is the leading cloud ERP for mid-market companies — a segment IBM does not serve well

Where IBM Beats Oracle

- IBM’s open-source philosophy (Red Hat) versus Oracle’s proprietary stack gives IBM a neutrality advantage

- IBM Consulting’s breadth across industries and technologies exceeds Oracle’s consulting capabilities

- IBM’s AI governance platform (watsonx.governance) has no direct Oracle equivalent for regulated AI deployment

- IBM’s quantum computing and research investment has no Oracle equivalent

6. SAP SE

The undisputed ERP leader — dominates enterprise process software

| FY2025 Revenue

$42.41 billion USD |

Cloud Revenue Share

~40% of total and growing |

| Market Position

#1 ERP globally |

Key Strength

Industry-specific ERP & SCM |

SAP is the world’s leading enterprise resource planning (ERP) software company, and while it does not compete with IBM in cloud infrastructure or consulting at the same scale, it is a direct competitor for enterprise software budgets — particularly in manufacturing, supply chain, and finance operations. SAP S/4HANA (the cloud-native ERP successor to SAP ECC) is the most widely deployed enterprise system of record in the world, running the core financial, procurement, and supply chain operations of the majority of the Global 2000.

The IBM-SAP relationship is both competitive and collaborative. IBM is one of SAP’s largest implementation partners — IBM Consulting has a dedicated SAP practice with thousands of certified SAP consultants helping enterprises migrate to S/4HANA. At the same time, IBM’s own enterprise software (automation, data integration, AI) competes for budget with SAP’s Business AI and SAP Integration Suite. The key insight: organisations that are heavily SAP-committed need IBM (or another SI) to implement SAP, but may choose SAP’s own tools over IBM’s for specific integration and analytics use cases.

Where SAP Beats IBM

- SAP S/4HANA is the definitive system of record for enterprise operations — IBM has no direct ERP alternative

- SAP’s industry cloud solutions (for automotive, utilities, retail) are deep and purpose-built verticals

- SAP Business Network (formerly Ariba) is the world’s largest B2B commerce network

- SAP Business AI is natively embedded in ERP workflows — IBM watsonx requires external integration

Where IBM Beats SAP

- IBM is a preferred SAP implementation partner — companies need IBM to get the most from SAP

- IBM’s hybrid cloud platform (Red Hat) is the preferred infrastructure for SAP S/4HANA cloud deployments

- IBM’s AI governance and automation tools complement SAP’s AI capabilities rather than replacing them

- IBM Research’s scientific depth in AI and quantum has no SAP equivalent

7. Cisco Systems

The networking and cybersecurity powerhouse — IBM’s rival in enterprise infrastructure

| FY2025 Revenue

$59.05 billion |

Security Revenue

~$5B+ annually |

| Market Position

#1 enterprise networking globally |

Key Move

Splunk acquisition ($28B, 2024) |

Cisco Systems is the world’s largest enterprise networking company and an increasingly formidable cybersecurity player following its $28 billion acquisition of Splunk in 2024 — the largest acquisition in Cisco’s history. Cisco competes with IBM primarily in two areas: enterprise networking infrastructure (where IBM’s infrastructure services overlap with Cisco’s hardware and software networking products) and cybersecurity (where IBM Security’s QRadar platform competes with Cisco’s portfolio of security tools now augmented by Splunk’s SIEM capabilities).

The Splunk acquisition has been the most consequential development in the IBM-Cisco competitive relationship. Splunk was one of the leading SIEM (Security Information and Event Management) platforms — and so is IBM’s QRadar. The combination of Cisco’s network visibility and Splunk’s security analytics creates a unified security operations platform that directly competes with IBM’s security division. IBM has responded by pivoting QRadar to cloud-native deployment and focusing on AI-driven threat detection through its X-Force threat intelligence platform.

Where Cisco Beats IBM

- Cisco is the definitive choice for enterprise networking hardware — switches, routers, and wireless — IBM has no equivalent

- Post-Splunk, Cisco’s security portfolio (SIEM + network visibility + endpoint) rivals IBM Security’s breadth

- Cisco’s Webex collaboration platform competes with IBM’s declining collaboration footprint

- Cisco’s partner ecosystem of VARs and resellers is unmatched in enterprise networking

Where IBM Beats Cisco

- IBM Security X-Force’s threat intelligence (monitoring 150B+ security events daily) is best-in-class for managed security services

- IBM’s AI-driven security operations (watsonx for security) is more mature than Cisco’s AI security offerings

- IBM Consulting provides end-to-end security strategy, design, and implementation that Cisco cannot

- IBM’s mainframe security capabilities for financial institutions have no Cisco equivalent

8. Hewlett Packard Enterprise (HPE)

IBM’s most direct rival in hybrid IT infrastructure and edge computing

| FY2025 Revenue

$34.30 billion |

Revenue Growth

~14% YoY |

| Key Platform

HPE GreenLake (as-a-service) |

Key Strength

Hybrid infrastructure & edge |

Hewlett Packard Enterprise (HPE) is perhaps IBM’s most direct competitor in the hybrid IT infrastructure market. Like IBM, HPE targets enterprises that need to run workloads across on-premises data centres, private clouds, and public clouds — and HPE’s GreenLake platform is the main competitor to IBM’s hybrid cloud and Red Hat OpenShift offerings. GreenLake offers a consumption-based, cloud-like payment model for HPE’s on-premises hardware — servers, storage, networking — allowing enterprises to avoid large capital expenditure while retaining control over their infrastructure.

HPE’s FY2025 revenue of $34.3 billion was boosted significantly by its $14 billion acquisition of Juniper Networks (completed 2024), which added enterprise networking and AI-driven networking capabilities. This positions HPE as a more complete infrastructure alternative to IBM, covering servers, storage, networking, and the software-defined management layer through GreenLake. For enterprises that want to stay on-premises or in a private cloud without committing to a specific public cloud vendor, HPE GreenLake and IBM’s hybrid cloud platform are the primary choices.

Where HPE Beats IBM

- HPE GreenLake’s consumption-based model gives enterprises cloud-like economics for on-premises infrastructure

- HPE’s server portfolio (ProLiant) is broader and more price-competitive than IBM’s Power Systems for general-purpose compute

- Post-Juniper acquisition, HPE offers networking + compute + storage in a unified hybrid platform

- HPE’s edge computing capabilities (Edgeline) are more mature than IBM’s edge offerings

Where IBM Beats HPE

- IBM’s Z mainframe is unmatched for high-volume transaction processing — HPE has no mainframe alternative

- Red Hat OpenShift is the #1 enterprise Kubernetes platform — HPE’s container story is weaker

- IBM Consulting’s scale and depth far exceeds HPE’s advisory services

- IBM’s watsonx AI platform is more developed and enterprise-ready than HPE’s AI offerings

9. Salesforce

![]()

The CRM and AI cloud leader — competing with IBM in enterprise AI and automation

| FY2025 Revenue

~$37.9 billion |

CRM Market Share

~22% globally (#1) |

| Agentforce Users

1B+ AI agents deployed (2025) |

Key Strength

CRM, AI Agents, Customer Data |

Salesforce is the world’s leading CRM platform and an increasingly aggressive competitor to IBM in enterprise AI. Salesforce’s FY2025 revenue of approximately $37.9 billion is generated through its Customer 360 platform — a unified suite covering sales automation, marketing, customer service, commerce, and analytics. The company’s strategic pivot to AI agents in 2025, through its Agentforce platform, positions it directly against IBM’s watsonx automation and AI assistants for enterprise process automation.

Agentforce — Salesforce’s platform for deploying autonomous AI agents that can handle customer service queries, sales outreach, and workflow automation without human intervention — has been one of the most discussed enterprise AI launches of 2025. IBM’s watsonx Orchestrate performs a similar function: AI agents that automate business workflows across enterprise applications. The battle for the ‘enterprise AI agent’ market is becoming one of the most important competitive dynamics of the next five years, and both IBM and Salesforce are investing heavily.

Where Salesforce Beats IBM

- Salesforce is the undisputed CRM leader — IBM has no competitive CRM product

- Agentforce’s customer-facing AI agents are more mature and more easily deployable than IBM’s equivalents

- Salesforce Customer Data Cloud provides a unified customer data platform IBM cannot match

- Salesforce’s AppExchange ecosystem (8,000+ apps) and partner network are unrivalled in the CRM space

Where IBM Beats Salesforce

- IBM’s AI governance (watsonx.governance) addresses regulatory compliance for AI in a way Salesforce does not

- IBM’s hybrid cloud and on-premises deployment capabilities give regulated industries more flexibility than Salesforce’s SaaS-only model

- IBM Consulting implements Salesforce — making IBM both a competitor and a key delivery partner

- IBM’s mainframe and back-end integration depth enables data flows that Salesforce’s platform cannot access directly

10. Infosys & TCS

India’s IT giants — the highest-volume competitors to IBM Consulting

| Infosys FY2025 Revenue

~$19.4 billion |

TCS FY2025 Revenue

~$30 billion |

| Combined Employees

~700,000+ |

Key Advantage

Cost-competitive delivery at scale |

Infosys and Tata Consultancy Services (TCS) are India’s two largest IT services companies and the most cost-competitive alternatives to IBM Consulting for large enterprise technology outsourcing and implementation engagements. Together, they employ over 700,000 technology professionals and offer services spanning application development and maintenance, cloud migration, ERP implementation, cybersecurity, and AI/ML development. Their fundamental competitive advantage is cost: both companies deliver high-quality IT services at a price point that IBM Consulting — with its higher-cost talent model — cannot match for volume, labour-intensive delivery.

TCS, with approximately $30 billion in FY2025 revenue, is the larger of the two and competes with IBM across banking, financial services, retail, and manufacturing. Infosys, at approximately $19.4 billion, is particularly strong in manufacturing, energy, and high-tech sectors. Both companies have invested heavily in AI capabilities and have launched dedicated AI consulting and implementation practices that compete with IBM’s watsonx services. Infosys Topaz (its AI-first IT services brand) and TCS AI Cloud Services are direct competitors to IBM’s AI consulting offerings.

Where Infosys/TCS Beat IBM

- Significantly lower cost per resource — crucial for labour-intensive IT outsourcing and application maintenance

- Massive talent pools in India enable rapid scaling of delivery teams that IBM cannot match at the same price point

- Strong relationships with enterprise IT procurement teams that prioritise cost efficiency over vendor IP

- Infosys and TCS are vendor-neutral — they implement IBM, SAP, Oracle, and cloud platforms without bias

Where IBM Beats Infosys/TCS

- IBM owns the technology — watsonx, Red Hat, Z systems — giving it unique leverage in technology-centric deals

- IBM Research provides scientific depth and intellectual property that TCS and Infosys must license or work around

- IBM’s relationships with C-suite executives (CEO, CTO, CISO) at Fortune 500 companies are typically more strategic than Infosys/TCS relationships, which often sit at CIO/VP level

- IBM’s quantum computing, mainframe expertise, and industry certifications in regulated sectors create barriers that IT outsourcers cannot easily replicate

Head-to-Head Comparison: IBM vs Top 10 Competitors

The table below summarises how each competitor compares to IBM across six key dimensions: revenue scale, cloud capability, AI platform, consulting depth, industry specialisation, and best use case.

| Company | FY2025 Rev. | Cloud Strength | AI Platform | Consulting | Best For |

| IBM | $67.5B | Hybrid Cloud (Red Hat) | watsonx ★★★★ | ★★★★ | Regulated industries, legacy modernisation |

| Microsoft | ~$280B | Azure ★★★★★ | Copilot + OpenAI ★★★★★ | ★★★ | Microsoft-centric enterprises |

| AWS | $115B+ | AWS ★★★★★ | Bedrock ★★★★ | ★★★ | Cloud-native, digital-first companies |

| Google Cloud | $50B+ | GCP ★★★★ | Gemini/Vertex ★★★★★ | ★★ | Data-intensive, AI-native workloads |

| Accenture | $70.7B | Multi-cloud neutral | Partner models ★★★ | ★★★★★ | Vendor-neutral transformation |

| Oracle | $61.0B | OCI ★★★ | Autonomous DB ★★★ | ★★★ | Oracle-heavy enterprises, ERP migration |

| SAP | $42.4B | SAP BTP ★★★ | Business AI ★★★ | ★★ | ERP-centric, manufacturing, utilities |

| Cisco | $59.1B | Networking ★★★★★ | AI Security ★★★ | ★★ | Network-centric, security-focused |

| HPE | $34.3B | GreenLake ★★★★ | HPE AI ★★ | ★★ | Hybrid IT, edge, private cloud |

| Salesforce | $37.9B | SaaS ★★★★ | Agentforce ★★★★ | ★★ | CRM, customer experience, AI agents |

| Infosys/TCS | $19-30B | Multi-cloud neutral | Topaz/AI Cloud ★★★ | ★★★★ | Cost-optimised IT outsourcing |

How to Choose: IBM or an Alternative?

The right answer depends entirely on your organisation’s starting point, industry, and strategic priorities. Here is a practical decision framework:

Choose IBM if:

- You run IBM Z mainframes and need to modernise without wholesale re-platforming — IBM is the only credible path

- You operate in a regulated industry (banking, insurance, government) where AI explainability, data sovereignty, and compliance are non-negotiable

- You want a hybrid cloud platform that runs consistently across on-premises, private cloud, and multiple public clouds — Red Hat OpenShift is the industry standard

- You need end-to-end technology consulting — from strategy through implementation — combined with the underlying technology (IBM Consulting + watsonx)

- You are investing in quantum computing for R&D or future competitive advantage — IBM Quantum is the world’s most advanced and accessible quantum platform

Choose an Alternative if:

- You are building cloud-native from scratch → AWS or Google Cloud offer superior breadth and developer experience

- Your entire stack is Microsoft (Office 365, Windows Server, Active Directory) → Azure + Copilot is the natural extension

- You need unbiased technology consulting with no IBM product agenda → Accenture, Infosys, or TCS

- Your core system is an Oracle or SAP ERP → those vendors’ cloud platforms are the most natural home for your workloads

- Your primary pain point is customer relationship management → Salesforce is unmatched in CRM

- You are optimising IT costs rather than transforming capabilities → Infosys or TCS offer equivalent capabilities at significantly lower cost

Frequently Asked Questions (FAQs)

Q: Who are IBM’s biggest competitors in 2025?

A: IBM’s biggest competitors depend on the business segment. In cloud infrastructure, IBM’s main competitors are Amazon Web Services (AWS, 29% market share), Microsoft Azure (20%), and Google Cloud (13%). In IT consulting and services, IBM Consulting competes primarily with Accenture ($70.7B revenue), Infosys, and TCS. In enterprise software and AI, IBM’s watsonx competes with Oracle Cloud, SAP, Salesforce Agentforce, and Microsoft Copilot. IBM’s most comprehensive competitor — the one that challenges it across the most segments simultaneously — is Microsoft.

Q: Is IBM still relevant in 2025?

A: Yes — and increasingly so. IBM posted $67.5 billion in FY2025 revenue (up 7.62% YoY), serves 95% of the Fortune 500, and has accumulated over $12 billion in generative AI bookings through its watsonx platform since launch. The company’s hybrid cloud strategy centred on Red Hat OpenShift is widely adopted in enterprise Kubernetes deployments. IBM is not relevant to every technology buyer, but for large regulated enterprises, financial institutions, and government agencies with complex legacy environments, IBM remains a primary technology partner. The company has successfully transitioned from a hardware company to a software and consulting company over the past decade.

Q: How does IBM compare to AWS and Azure in cloud computing?

A: IBM competes differently from AWS and Azure: it focuses on hybrid and private cloud rather than public cloud market share. AWS (29% global cloud share) and Azure (20%) dominate public cloud infrastructure — IBM’s public cloud is not competitive at that scale. IBM’s cloud advantage is in hybrid environments: Red Hat OpenShift is the #1 enterprise Kubernetes platform and runs seamlessly across on-premises, AWS, Azure, and Google Cloud simultaneously. IBM targets enterprises that need to keep some workloads on-premises (for regulatory, latency, or data sovereignty reasons) while connecting to public cloud services — a use case the hyperscalers’ own tools serve less effectively.

Q: What is IBM watsonx and how does it compare to competitors?

A: IBM watsonx is an enterprise AI platform launched in 2023, comprising three components: watsonx.ai (model training and deployment, including IBM’s own Granite models and third-party models), watsonx.data (a data store for AI), and watsonx.governance (AI transparency, risk management, and regulatory compliance). By early 2026, watsonx had accumulated $12+ billion in generative AI bookings. It competes most directly with Microsoft’s Azure OpenAI Service and Copilot (for enterprise AI deployment), Google Vertex AI (for model training and serving), Amazon Bedrock (multi-model AI platform), and Salesforce Agentforce (for AI agent workflows). IBM’s differentiator is AI governance and explainability — particularly important in regulated industries where AI decisions must be auditable and traceable.

Q: What happened to VMware as an IBM competitor?

A: VMware — previously one of IBM’s most direct competitors in virtualisation — was acquired by Broadcom in November 2023 for $61 billion. Following the acquisition, Broadcom restructured VMware’s business model, moving to subscription-only pricing and discontinuing many standalone VMware products. This restructuring has pushed many VMware customers to evaluate alternatives, including Red Hat OpenShift (IBM) and Azure Arc (Microsoft), for their virtualisation and hybrid cloud needs. VMware’s competitive relevance to IBM has shifted significantly post-acquisition.

Q: How does IBM Consulting compare to Accenture?

A: IBM Consulting and Accenture are the two most frequently compared technology consulting firms for large enterprise transformation projects. The key differences: Accenture is larger (750,000+ employees vs IBM Consulting’s ~160,000) and is vendor-neutral, recommending the best technology from any vendor without an in-house product agenda. IBM Consulting, by contrast, combines consulting with IBM’s own technology stack (watsonx, Red Hat, Z systems), which can be an advantage (integrated solution) or a perceived conflict of interest (recommending IBM products). For pure technology-agnostic consulting, Accenture is typically preferred. For engagements that involve IBM infrastructure or AI platforms, IBM Consulting’s integrated approach delivers unique value.

Q: What is IBM’s competitive advantage over its rivals?

A: IBM’s primary competitive advantages in 2025 are: (1) Red Hat OpenShift — the world’s leading enterprise Kubernetes platform and the foundation of IBM’s hybrid cloud strategy; (2) IBM Z mainframes — the only viable platform for the transaction volumes processed by the world’s largest banks and the irreplaceable core of many large financial institutions; (3) IBM watsonx.governance — the most mature enterprise AI governance platform in the market, critical for regulated AI deployment; (4) IBM Research — 3,000+ researchers across 12 global labs, producing foundational IP in AI, quantum computing, and materials science; and (5) Fortune 500 relationship depth — 95% of the world’s largest companies are IBM clients, creating an incumbency advantage that is extremely difficult for competitors to displace.

Q: Is IBM or Accenture better for digital transformation?

A: The answer depends on whether the transformation requires IBM technology. If you are modernising an IBM mainframe environment, deploying watsonx AI, or migrating to Red Hat OpenShift, IBM Consulting’s integrated approach — where the consulting team knows the technology stack intimately — provides a meaningful advantage. If the transformation is technology-agnostic (for example, choosing and implementing the best combination of cloud, ERP, CRM, and data platforms from multiple vendors), Accenture’s vendor-neutral model and greater scale (750,000+ employees) often make it the better choice. Many large enterprises use both simultaneously — Accenture for strategic advisory and IBM Consulting for IBM-specific technology implementation.

Q: What is IBM’s quantum computing competitive position?

A: IBM is the world’s leading provider of accessible quantum computing through IBM Quantum, which operates the largest fleet of quantum computers available via cloud access globally. With 100+ qubit systems accessible to over 500,000 registered users and 250+ member organisations in the IBM Quantum Network, IBM leads all competitors in quantum accessibility and ecosystem development. Microsoft, Google, and IonQ are the primary quantum computing competitors. Google claimed ‘quantum supremacy’ with its Sycamore processor in 2019, and Google’s Willow chip (2024) achieved significant milestones, but IBM’s quantum computing is more enterprise-accessible and deployment-ready. No IBM competitor yet offers comparable quantum hardware access at IBM’s scale.

Q: Which IBM competitor is best for small and medium businesses (SMBs)?

A: IBM primarily serves large enterprises and is generally not the right choice for SMBs. For small and medium businesses, the better alternatives are: Microsoft Azure (best for Microsoft-centric SMBs through Microsoft 365 and Azure’s SMB-friendly pricing), AWS (for cloud-native SMBs with technical teams), Salesforce (for CRM and customer management), SAP Business One or NetSuite/Oracle (for ERP needs), and Cisco Meraki (for simplified networking). IBM’s minimum engagement sizes and enterprise-focused products make it economically impractical for most SMBs. IBM’s consulting and technology platforms are optimised for complexity and scale that SMBs typically do not encounter.

Conclusion: IBM’s Competitive Position in 2025

The technology competitive landscape IBM operates in is more crowded and more capable than at any point in the company’s 114-year history. AWS, Azure, and Google Cloud have built public cloud empires that dwarf IBM’s cloud revenue. Accenture has more consultants. Oracle and SAP own the enterprise software categories IBM helped create. Salesforce has reinvented enterprise CRM and is aggressively expanding into AI agents. Infosys and TCS offer comparable delivery at dramatically lower cost.

Yet IBM’s FY2025 revenue of $67.5 billion and its $12+ billion watsonx AI bookings tell a different story: there is a very specific market that IBM uniquely serves — large, regulated enterprises with complex legacy environments that need to modernise carefully rather than rebuild from scratch. For these organisations, the combination of Red Hat’s open-source hybrid cloud, IBM’s mainframe expertise, watsonx’s AI governance capabilities, and IBM Consulting’s industry depth represents a value proposition that no single competitor can fully replicate.

The practical takeaway for any organisation evaluating IBM versus its alternatives: start with your specific use case, your existing technology estate, and your industry’s regulatory requirements. IBM is not the right choice for everyone — but for the enterprises it is designed to serve, it remains one of the most capable and defensible technology partners in the world.

Also Read: Who are Supermicro’s Top Competitors in Technology Industry?

To read more content like this, subscribe to our newsletter

Go to the full page to view and submit the form.