Since his acrimonious exit from Flipkart in 2018, Sachin Bansal has made some big moves to prepare a major banking play with Navi Technologies. While at Flipkart Bansal used acquisitions to grow the business, Navi’s acquisitions have been operations-centric to fulfil key regulatory requirements for banking. But even as it looks to revolutionise banking service with tech, can Navi also fight back competition from traditional heavyweights and earn the trust of consumers?

Walt Disney once said, “The way to get started is to quit talking and begin doing.”

That’s what Sachin Bansal did. Soon after his exit from Flipkart, the cofounder and former chairman, switched gears to motor along on the quest to turn his long-term ‘Big Billion’ vision into a reality. Even as the Flipkart dream ended for Sachin Bansal, he had his eyes set on the next big thing.

This restlessness pursuit for something new is seen in the fact that since his exit from Flipkart, there have only been a handful of months when Bansal has not invested in or acquired a business – primarily for his new startup Navi Technologies. Even during the lockdown, the Navi founder and CEO infused INR 3,000 Cr into his own company and launched an app for personal loans.

Like Navi, which has acquired a slew of companies in the past two years, Flipkart too was built on a stack of acquisitions. Starting with Weread in 2010, to Letsbuy in 2012, Myntra in 2014 and Phonepe and Jabong in 2016, the ecommerce giant closed over a dozen acquisitions en route to becoming the market leader and take on Amazon and other contenders.

Along the way, Bansal infused his big billion vision into Flipkart – which is evidenced in Flipkart’s ultra-successful seasonal Big Billion Day sale and the short-lived Billion smartphone brand. While Flipkart has often been termed as the biggest success story for Indian startups and investors, for Bansal, it remained ‘an unfinished business’, considering the blueprint of $100 Bn plan he had laid out for ‘Flipkart 3.0’ as author, journalist Mihir Dalal wrote in his book Big Billion Startup.

However, since his acrimonious and untimely exit from Flipkart in 2018, Bansal quickly shifted his focus from consumer tech and ecommerce to banking, financial services and insurance (BFSI). With an addressable base that pretty much covers the entire Indian population of 1.3+ Bn people, Navi might finally be the big billion idea that Bansal has craved.

At Navi too, acquisitions have been a key strategy – the primary difference between Flipkart’s acquisitions and Navi’s is the stage at which they have come. While Flipkart was already on its way to becoming an ecommerce giant when it acquired Myntra, Jabong and PhonePe, Navi acquired companies even before the launch of the product or service. As we will see, a lot of this has to do with the banking and financial services sector and its peculiar and specific needs that Navi and Bansal are looking to fulfil.

Bansal has made over two dozen investments and acquisitions in personal capacity and through Navi Technologies (formerly BAC Acquisitions). Having invested close to $1 Bn in various companies with a major chunk in Navi, he registered a slew of companies from December 2018. From DHFL General Insurance to Essel MF, the operations-centric acquisitions at Navi are clearly of a different nature than Flipkart’s growth-focused acquisitions. These acquisitions don’t bring brand value, a huge user base or technology to Navi, instead, they are focussed on helping Navi enter the banking sector.

But save for the Navi personal loans app which was launched officially in late June, Bansal is yet to launch any major product under the Navi umbrella. Meanwhile, Navi General Insurance, a makeover of DHFL General Insurance acquired earlier this year has laid off around 40 employees citing headquarter relocation from Mumbai to Bengaluru.

So can Bansal, who could not fulfil his idea of turning Flipkart into a $100 Bn company, do it with Navi?

Tackling The BFSI Beast

Compared to the $64 Billion Indian ecommerce which is just a fraction of the overall retail market, the BFSI sector is simply massive. The $1.86 Trillion market size of the sector in India offers a much bigger ladder to climb.

But while ecommerce and Flipkart matured together and in unison, Navi is entering the world of legacy finance and money.

So the bigger opportunities also come with massive and sometimes insurmountable challenges. Unlike Flipkart, where there was hardly any major competition until Amazon entered the Indian market, the BFSI sector is filled with large public and private companies, legacy institutions as well as hundreds of tech startups offering lending, payments, insurance, investments and other financial services.

It does not matter how much one invests in the fintech sector, it’s always going to be a shoestring budget compared to the money that has gone into the overall banking and finance industry. And when it comes to Bansal’s vision of providing end-to-end integrated BFSI services, the bar is even higher. The veteran in consumer tech is a novice in the BFSI sector – will this be a story of David vs Goliath?

Earlier this year, in an interview with CNBC, Bansal said the answer lies in technology and catering to other services besides banking, savings and payments. He believes that the quality of service varies drastically between classes and some services just cannot be improved without technology.

Bansal is arguably spot on. India’s legacy banking companies struggled to integrate state-of-the-art systems into their existing infrastructure.

They have experimented with blockchain, machine learning, AI, API banking and open banking technologies in isolation and in pilot projects, but the scale of adoption is low because of red tape, the lack of talent and regulatory shuffling.

Even full-fledged neobanking services, that can work without the support of legacy banking institutions, are a dream in India owing to the existing partnership-based regulatory burden. But Bansal wants to do away with the partnership model once and for all.

Setting Up Navi: From A Diversified Portfolio To Concentrated Investments

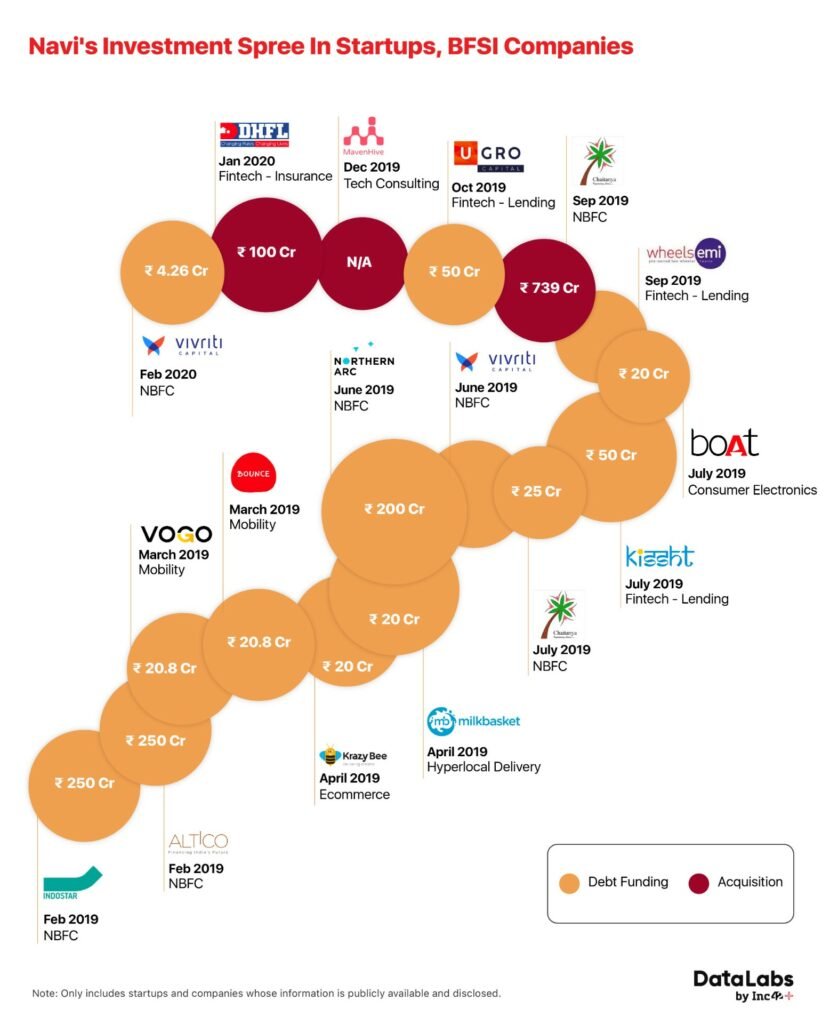

Bansal’s investments can clearly be divided into two eras – with Flipkart and after Flipkart. During his Flipkart tenure, Bansal invested in around 20 startups as an angel and had quite a diversified portfolio which includes edtech startups such as Unacademy, English Dost, deeptech startup Inkers, foodtech startup Spoonjoy, media and entertainment Inshorts, spacetech TeamIndus, healthtech startup SigTuple to EV startups Ather Energy and Ola.

While these were angel investments made in his personal capacity, Bansal along with his Flipkart cofounder Binny Bansal had even set up SABIN (SAchin + BINny) Advisors in December 2017. The idea was to explore investment opportunities in early-stage startups. However, soon after the Flipkart acquisition by Walmart, SABIN had to put its plans on hold. Binny Bansal and Sachin Bansal parted ways right after the Walmart acquisition and currently SABIN Advisors is in the process of being struck off.

Immediately after exiting Flipkart, Sachin Bansal set up BAC Acquisitions (Renamed to Navi Technologies later) in December 2018 for investments and acquisitions purposes, particularly in BFSI. Besides, he also continued to invest in mobility and other startups individually as well. In January 2019 he invested INR 650 Cr in Ola, acquiring around 2% of the company’s PE. After Flipkart, Bansal has invested in 18 companies overall, personally as well as through BAC Acquisitions.

However, the nature of investments in the post-Flipkart era has also changed. Barring a few, all the investments have not only been made in BFSI space but have also been made via debt funding unlike the equity-based angel investments during the Flipkart era.

Interestingly, many of the investments such as in Bounce, VOGO and Krazybee were initially made in his personal capacity, later transferred to BAC Acquisitions / Navi Technologies in assets.

Among the acquisitions by Navi are the likes of Essel Mutual Fund, Essel AMC, Chaitanya Rural Intermediation Development Services (CRIDS) along with its wholly-owned subsidiary Chaitanya India Fin Credit Pvt Ltd, DHFL Insurance and Mavenhive.

Some of the acquisitions such as Essel Mutual Fund and Essel AMC have not been approved by SEBI. The acquisitions, however, have been cleared by Competition Commission of India (CCI).

With Navi, the focus has been on tech-enabled banking and financial services, a seamless integration of the neobanking model with traditional banking services and assurance. In order to acquire domain expertise as well, Sachin Bansal in his second innings has collaborated with fellow IIT Delhi alumnus Ankit Agarwal, a banker by profession.

Despite the array of acquisitions and investments, Bansal and Navi have not yet touched payments and stockbroking yet.

In contrast to his planning of hotfooting into BFSI, the regulatory hurdles and the lockdown have slowed down Navi’s momentum. While Bansal has managed to get SEBI approval on the registration of Navi Investment Advisors as an advisory, applications for the approval of Essel Mutual Fund acquisition and a new license for Chaitanya Fin Credit to operate in mutual funds are still pending.

However, the major hurdle for Bansal remains getting the universal license. Speaking to Inc42, a corporate lawyer said that the RBI and SEBI have made the license approval route a more stringent process in recent years. However, these steps have been taken simply to ensure the security of customer investments. The eligibility of the applicants such as the promoter’s profile, shareholding details and others are closely scrutinised to examine whether the promoters have the ability to carry on the business, and whether the company is completely dependent on promoters alone.

Could the lack of supporting documents lead to the cancellation of applications? No, the lawyer said – but regulators in such cases do actively engage with the promoters and the latter is given further time to fill any gaps in their application.

The Investors Backing Navi

Besides acquiring firms, Bansal has also been in talks with venture capitalists and institutional investors for fundraising. The World Bank’s investment arm International Finance Corporation (IFC) has already proposed to acquire 4.5% stake in Navi for $30 Mn.

The investment has been done in lieu of Chaitanya Rural Intermediation Development Services Pvt. Ltd’s (CIFCPL) application for a universal banking license. According to the IFC’s disclosure report, IFC’s investment in Navi will help support the transformation of CIFCPL into a technology-led universal bank or Navi Bank (which the IFC called ‘The Project’) to provide mass-market banking solutions for individual and micro, small and medium enterprises (MSME) and select corporates.

Bansal on the investment had then commented,

“Building a universal bank is a reflection of our commitment to provide financial services to those who need them most. Our vision is to go beyond what hitherto has been broadly defined as ‘financial inclusion’ and provide access to formal financial services using technology that people can use intuitively and easily.” – Sachin Bansal

Besides IFC, private equity firm Gaja Capital led by Gopal Jain has also invested INR 204 Cr in Navi Technologies and has acquired 1.45 Cr shares, according to regulatory filings. Over 22 people currently hold either private or preferential equities in the company.

As part of its acquisition deal, the company Navi technologies has also allotted 16,54,748 and 2,80,038 shares to the founders of CIFCPL Samit Shetty and Anand Rao respectively.

Also Read: Robinhood – The Financial App That Makes Investing Easy

Hold On, There’s Turbulence Ahead

India’s fintech revolution and the multi-trillion-dollar market opportunity in the sector have made BFSI a lucrative option for tech entrepreneurs.

However, the industry remains heavily guarded by capital and regulatory requirements as far as the entry is concerned and the recent downfall of several public sectors and private banks have worried investors as well as consumers

Fintech companies such as Paytm, Razorpay, Instamojo and others, however, have made inroads into insurance, lending and investment spaces pushing the envelope for fintech innovation. Even non-fintech companies such as Ola and Flipkart have entered the fintech sector through various services.

Bansal however has an entirely different gameplan and so are his challenges. While entering the BFSI, Bansal has avoided competing with Flipkart’s PhonePe and other payments companies where most of them are already the early adopters of UPI and other standards.

Interestingly, if we look at the acquisition pattern, while Bansal opted to invest in the latest tech-savvy companies, the acquisition has been rather focussed on meeting the criteria set by the RBI and other regulatory authorities. For instance, for a universal banking licence, a company needs to have at least 10 years of domain experience. CIFCPL fulfils that criteria perfectly.

However, the lending market equations are fast changing. The account aggregator (or AA) standard will revolutionise the way user consent is currently taken and will help NBFCs, banks, insurance companies access user data seamlessly with the right consent. This is expected to reboot the entire BFSI sector, experts believe.

While most of the startups, banks have already started adopting AA framework for the seamless data sharing with user consent, Bansal’s existing companies seem to be falling behind in the race.

For a long time, ecommerce companies have been criticising the Indian government for not having a dedicated ecommerce policy. However, unlike the consumer tech, the BFSI sector in India is heavily guarded by regulatory authorities which include RBI, Securities Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI) and Pension Fund Regulatory and Development Authority (PFRDA).

With some acquisitions yet to get the green light and licences stuck with the SEBI and the RBI, Navi is technically still not prepared to enter the game despite being close to achieving the unicorn status.

However, getting a license is only about getting started and the banking game is set to become much murkier for Bansal than the experience of growing and scaling-up the ecommerce sector with Flipkart. While public sector banks have been notoriously infamous for their opacity, a slew of private sector banks have been found to have major weaknesses and hence had to bear the brunt of the RBI and the market.

Can Sachin Bansal manage to bring in more transparency in the game to win the trust of investors through tech? That will be the biggest challenge once the licences are in place.

Bansal aims to leverage tech to change the face of the age-old BFSI behemoth. He might be right to a large extent; however, technology alone can’t fix all the BFSI issues. For instance, YES BANK was among the firsts to offer UPI payments and also entered API banking, facilitating the issuance of a commercial paper (CP) of INR 100 Cr using blockchain technology for Vedanta, a natural resources conglomerate. The bank was at the forefront of tech adoption, yet had to face an RBI moratorium because of mismanagement.

What makes banking and financial services tough for Navi are the end mile gaps that Bansal wants to bridge. So far, banks have been unable to cater to the consumers at the level at which NBFCs and payments apps do. Bansal wants to change that through intuitive customer service and an automation-led experience.

Right from creating a whole new consumer base for itself to competing with banks as well as NBFCs, Navi is likely to face the question of controlling its burn rate in the next few months, which will impact the survivability of the company. While part of the issue could be resolved by more share issuance or subscriptions, other issues such as resolving critical bugs in real-time and achieving the operational scale that banks have built over centuries in a matter of months.

Having faced a similar situation while launching the Big Billion sale on Flipkart in 2014, and later having written a long apology email to its consumers, Bansal is completely aware of how bad user experience can make or break a company, and if it has to do with money and savings, it’s all the more sensitive.

So in the banking sector, the repercussions compared to Flipkart could be much more. Bansal had earlier explained the difference between the two.

“If you are a Flipkart or a taxi app or a food delivery app, for you that transaction – you have to deliver that transaction in the best possible manner, with the most cost-efficient manner, best customer experience but in banking and financial services, what I found is that relationship is a multi-year relationship, it is not about just making a transaction happen or getting an account opened or getting a fixed deposit opened or selling an insurance policy, it is a very long-term relationship. So that mindset shift is something that is the biggest thing that I have learnt,” he said in an interview.

And this focus on building a tech platform for a multi-year relationship is seen in the hiring by Navi. It has followed the 80:20 pattern, where only 20% of the people come from a core financial services background.

There are other issues too that could impact Navi’s life ahead. Some of Sachin Bansal’s investments have not gone well as he may have desired. For instance, Bansal’s personal investments, English Dost has virtually shut down its operations.

Secondly, NBFCs have not exactly been a growth sector, especially due to the ongoing and prolonged liquidity crunch. Navi’s investments have been aggressively made in NBFC and lending space. NBFCs such as Altico Capital where Bansal had invested INR 250 Cr via debt in Feb, 2019 went rogue right after a few months. Altico Capital India defaulted on its debt obligations December 2019 to the tune of INR 138.31 Cr. The brand acquisition choice too, as experts have indicated, has not been great. For instance, DHFL General Insurance – which Bansal immediately rebranded to Navi General Insurance – has the legacy of Dewan Housing Finance Corporation (DHFL), a troubled lender facing bankruptcy.

Navi: The Inorganic Bank

India’s BFSI sector faced some unprecedented challenges in recent years. Banking is a sector that is the engine of the economy and any lag here, has a ripple effect as seen in the Indian economy in the past two years. When the economy is growing healthily, the gaps in the system can be overlooked, but in a crisis situation, the problem becomes difficult and can be resolved only through pumping in resources, liquidity, capitalization and big reforms, Professor M.S. Sriram, faculty and chair, Centre for Public Policy at IIM, told Inc42.

“We are in a peculiar stage where both the lead and the lag are under stress and therefore banking will go through a prolonged period of low business and stress,” Prof Sriram added.

In such a situation, is it wise to enter the sector entirely through the acquisition route? A PwC partner told Inc42 on the condition of anonymity that it would be better to read the market in an entrepreneurial way and adapt to market changes and respond, before going for an acquisition spree. Though they did agree that the acquisition route allows faster scaling than the organic route like building everything from scratch.

So perhaps acquisition was the only way for Navi and Bansal. Bansal had limited options other than acquisitions given the RBI rules on promoters. Further, according to the RBI rules, Bansal may have to dilute more shares in the near future for the universal banking license.

Besides meeting the legal requirements, a complete makeover of all the acquired companies, their brands and products are underway. For Navi, it is crucial as some of the companies such as Essel MF funds as well as DHFL have not been performing well in the market and need an image makeover.

Is it the right time to enter India’s BFSI? Experts have divided opinions. Many experts that Inc42 spoke to said that it’s not the best time to enter the BFSI sector, some fintech startup founders have suggested otherwise that work-from-home has brought technology to the centre stage, so perhaps banking also is ready for the big shift.

An executive who is heading one of the largest AMCs in the world told Inc42, “As the lockdown has forced every to operate from their homes via mobiles. There is a huge opportunity for tech platforms to redesign the existing products and services accordingly.”

Banks like YES BANK, one of the largest private sector banks going through a rough time, open up some opportunities for new entrants too. IIM Bangalore’s Sriram said, “The new entrants have the benefit of not having the lag effect if they are a greenfield project. Unfortunately, the new entrants like Navi are in a brownfield project and not a greenfield project and therefore there will be challenges for them as well.”

Demonetisation once pushed people to make payments online. Lockdown thus may force both BFSI companies as well as consumers to go mobile. Hence, in such a situation, most of the players will have to start the race from scratch – something that banks had to do during demonetisation as well, which opened up the market for fintech startups. This is where Sachin Bansal and Navi could have a chance to score over leaders of the game.

The key point would be not just acquiring and running them as separate companies but integrating all the services under one platform. With the help of ML and AI, this will provide immense data to the company in order to understand the exact customer needs and will help the company to delve deeper into their profiles making more precise recommendations to the consumers such as their health insurance needs, investment needs and so on. This is something that companies have not really cracked yet.

Banking On Technology To Solve Trust

‘The idea appears to be to offer the entire gamut of neobanking services, In India, you can’t have it without a universal banking license,’ said Sriram.

While he believes that there is scope for technology to redefine the game, he added, “We have not seen the unfolding of this story in all its complexities. This is a space to watch,”

Lalit Keshre, cofounder and CEO of Groww, a Bengaluru-based platform offering investing money in mutual funds, SIP etc told Inc42 that technology has two broad roles to play – one to improve the user experience and second to reduce the cost.

Onboarding and acquiring users has been a costly affair so far, said Keshre. From regulatory compliance to KYC to payment processors and gateways and more, there is a cost involved at every step, which technology has helped reduce and has been optimising it further. This has helped customise products for last mile-consumers effectively.

However, the existing cost is still high and there is room to change this. Reducing costs could be the biggest role for tech and could result in the exponential rise of customers, feels Keshre.

Technology is more than just enablement for the BFSI heavyweights these days and is taking the centre stage, playing a key role in helping building trust among consumers and adding value to the banking service.

In the BFSI sector, trust is the key factor, above all. People are giving away their hard-earned money to the companies especially banks, insurance and asset managers. Hence, trust is of paramount importance. Earlier, banks enjoyed greater trust by default, however, things have changed now after years of non-performing assets piling up and banks seeing scams and defaults.

There is always a lot of concern about the sustainability of new BFSI companies. Even if it’s an NBFC, people are usually careful about approaching a new bank for services. It takes years to build trust. So people need to be confident about trust. However, with YES Bank, PMC Bank, the trust factor has eroded. Perhaps it’s time for a change and if Sachin Bansal can build trust in Navi, it might just be the bank for a billion Indians.

Source: IIM Bangalore Website