Last Updated on June 1, 2026 by Team TBH

Grab at a Glance (2026)

Introduction: What Is Grab?

If you live or work in Southeast Asia, Grab is as fundamental to daily life as a mobile phone. It books your ride to the airport, delivers your lunch, moves your parcels, and — increasingly — holds your savings, approves your loan, and processes your insurance claim. In a single app, it bundles the functions of Uber, DoorDash, PayPal, and a digital bank, tailoring each to the specific needs of one of the world’s most diverse and fast-growing regions.

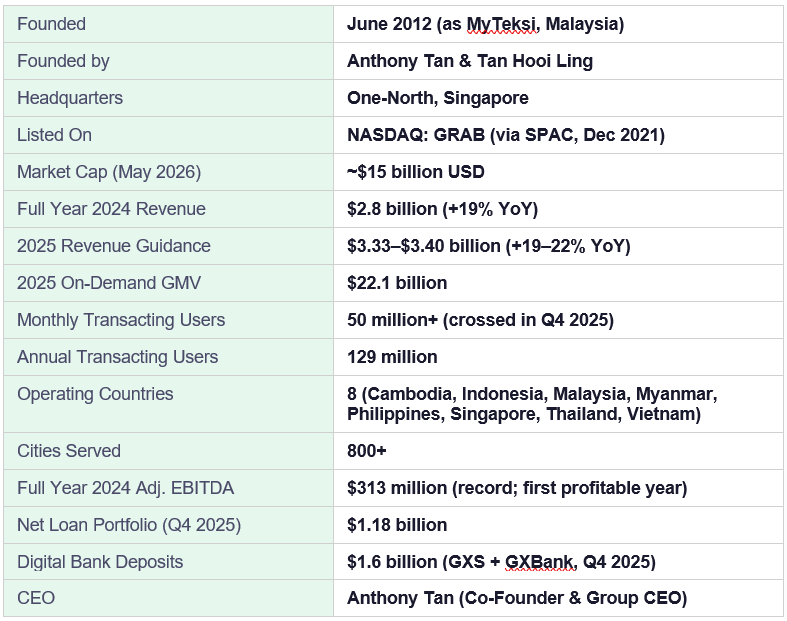

Grab Holdings Limited (NASDAQ: GRAB) is Southeast Asia’s leading superapp, operating across eight countries and more than 800 cities. As of the end of 2025, Grab crossed 50 million Monthly Transacting Users (MTUs) — a milestone that confirmed it as the go-to platform for hundreds of millions of Southeast Asians going about their everyday lives. The company posted its first-ever full-year net profit in 2025, marking a pivotal transition from a growth-at-all-costs startup to a sustainable, profitable technology business.

The story of how a Harvard Business School student’s observation about Southeast Asian taxi rides grew into a $15 billion company is one of the defining startup narratives of the 21st century. Understanding Grab means understanding Southeast Asia’s digital economy — its scale, its potential, and the unique challenges of building technology that works for 700 million people across wildly different markets.

Founding Story: From MyTeksi to a Regional Superapp

The Harvard Business School Idea

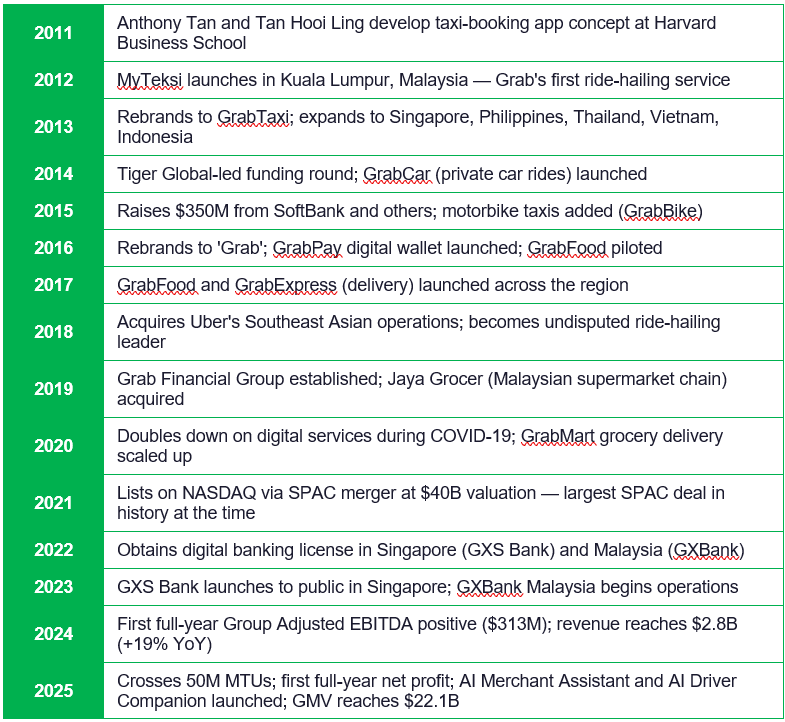

The origin of Grab traces back to a Harvard Business School competition in 2011. Anthony Tan, a Malaysian student from a prominent automotive family (his grandfather founded Tan Chong Motor), submitted a business plan for a taxi-booking app for Malaysia. His classmate and co-founder Tan Hooi Ling (a graduate of the University of Cambridge, previously at McKinsey) helped him develop it. The plan won second place in the competition — but first place in the real world.

Anthony Tan had grown up watching his family navigate Malaysia’s automotive industry, but it was the chaotic, unreliable, and often unsafe experience of hailing a taxi in Kuala Lumpur that convinced him there was a genuine problem to solve. In cities where GPS navigation was unreliable, taxis often refused short-distance rides, and passengers — particularly women travelling alone at night — felt unsafe, a technology-enabled ride-hailing platform could transform urban mobility.

MyTeksi (2012): The First Ride

In June 2012, Anthony Tan and Tan Hooi Ling launched MyTeksi in Kuala Lumpur, Malaysia. The app connected passengers with licensed taxis through a simple smartphone booking interface. In a market where taxi drivers were resistant to technology and passengers had low trust in the industry, the founders spent months on the ground at taxi stands, physically meeting drivers, explaining the app, and building the trust that would underpin early adoption.

The name ‘MyTeksi’ blended the Malaysian possessive ‘my’ with ‘teksi’ — the Malay word for taxi — signalling clearly that this was a local solution built for local needs. Early traction was strong enough that by 2013, the founders began thinking beyond Malaysia’s borders.

GrabTaxi and Regional Expansion (2013–2015)

In 2013, MyTeksi rebranded to GrabTaxi to reflect its regional ambitions, and began expanding into Singapore, the Philippines, Thailand, Vietnam, and Indonesia. Each new market came with unique regulatory environments, local taxi associations with different relationships to technology, and consumer behaviour patterns shaped by distinct cultures and income levels. Grab built localised teams in each country — a strategic decision that distinguished it from more centralised competitors.

A crucial inflection point came in 2014, when Tiger Global Management led a significant funding round that gave GrabTaxi the capital to expand aggressively. Competition was intensifying: Uber had entered Southeast Asia, and Indonesia’s own Gojek was emerging as a formidable local challenger.

Grabbing Uber’s Southeast Asia Operations (2018)

In March 2018, Grab achieved a landmark competitive victory: it acquired all of Uber’s Southeast Asian operations in exchange for a 27.5% stake in Grab. The deal — which included Uber’s driver-partners, rider base, and local infrastructure across all eight countries — made Grab the unambiguous market leader in ride-hailing across the region overnight. Uber’s withdrawal from Southeast Asia was a clear signal that the regional superapp model, built on local knowledge and multi-service integration, had won.

“We started out wanting to solve a real problem — the experience of getting a taxi in Southeast Asia was broken. What we didn’t fully anticipate was how much more broken the rest of the ecosystem was — and how much we could do to fix it.” — Anthony Tan, Group CEO, Grab

Key Milestones in Grab’s History

Grab’s Business Model: The Superapp Flywheel

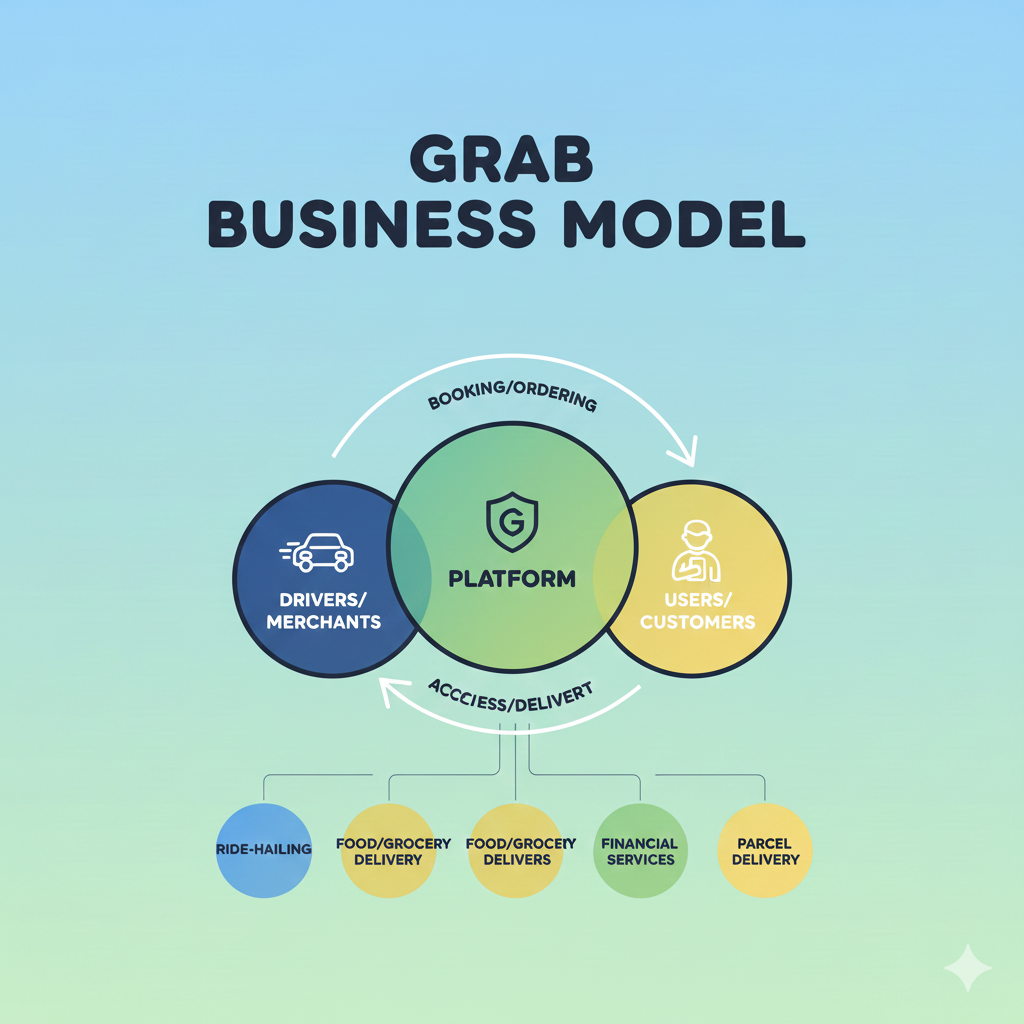

Grab’s business model is built on a superapp architecture: a single, unified platform through which users access a growing portfolio of services without switching apps. This is not merely a convenience — it is a structural competitive advantage. Every time a user adds a second or third Grab service to their daily routine, they become significantly harder to displace. Grab’s own data shows that multi-service users spend four times more on the platform than single-service users.

The flywheel works like this: more users attract more merchants, drivers, and financial service partners; a larger supply network produces faster, more reliable, and cheaper services; better services attract more users. As the flywheel spins faster, the economics improve, the moat deepens, and the cost of switching to a competitor — even one with a lower price on a single service — becomes too high for most users.

1. Mobility Services (Ride-Hailing)

Ride-hailing remains Grab’s foundational service and still drives the majority of platform transactions. Grab offers private cars (GrabCar), taxis (GrabTaxi), motorcycles (GrabBike), premium cars (GrabLux), shared rides, and chartered corporate transport. Grab operates as a marketplace, connecting passengers with driver-partners and charging a commission (typically 15–25% depending on market and ride type). Crucially, Grab does not own vehicles — its asset-light model mirrors Uber’s global playbook but is adapted for Southeast Asia’s diverse vehicle preferences.

In Malaysia and the Philippines, Grab commands over 90% ride-hailing market share. In Indonesia — its largest market — Grab leads with approximately 50% share, ahead of Gojek. Across the region, Grab is estimated to be 3 to 3.5 times larger than its nearest competitor.

2. Deliveries (Food, Grocery & Packages)

GrabFood has grown into one of Southeast Asia’s largest food delivery platforms, connecting users with hundreds of thousands of restaurants and hawker stalls. The pandemic accelerated this segment dramatically, and Grab has maintained its position even as dining-out recovered. GrabMart (grocery and convenience delivery) and GrabExpress (same-day parcel delivery) round out the deliveries business. Grab charges restaurants commission fees (typically 15–30%), and customers pay delivery fees and service charges.

In Malaysia, Grab also operates physical grocery retail through Jaya Grocer and Everrise — a notable departure from the pure digital model and a signal that Grab sees offline-to-online retail integration as a key differentiator.

3. Financial Services (Grab Financial Group)

Financial services is Grab’s fastest-growing and most strategically important segment. The founding insight was simple: Southeast Asia is massively underbanked. Fewer than half of adults in many Southeast Asian markets have a traditional bank account — but almost all have a smartphone. Grab’s financial services arm was designed to serve this population with products calibrated for their income levels, credit profiles, and transaction habits.

Grab Financial Group operates across five verticals: GrabPay (digital wallet and payment processing), GrabInsure (insurance products), GrabInvest (wealth management products), lending (micro-loans for driver-partners, merchants, and consumers), and digital banking through GXS Bank (Singapore) and GXBank (Malaysia). By Q4 2025, digital banking deposits across both banks had reached $1.6 billion — up from $1.2 billion a year earlier — and the net loan portfolio had doubled to $1.18 billion.

4. Enterprise and Advertising Services

Grab also generates revenue from enterprise services — providing logistics, last-mile delivery, and fleet management solutions to large corporations and government agencies. Its advertising platform, GrabAds, allows brands to reach Grab’s highly engaged user base with contextually relevant placements across the app. As Grab’s user data assets deepen, GrabAds is becoming a meaningful revenue contributor and a competitive moat for merchant retention.

Revenue Streams: How Grab Makes Money in 2026

Grab’s revenue model is deliberately diversified, a deliberate strategy to reduce dependency on any single vertical and to capture more value from each user relationship over time. In 2024, Grab’s total revenue reached $2.8 billion — a 19% year-on-year increase. For 2025, the company guided for $3.33–$3.40 billion in revenue, representing 19–22% growth.

1. Commission Fees

The largest revenue component is commissions. For every ride completed, food order delivered, or grocery parcel dispatched, Grab takes a percentage of the transaction value from the service provider (driver, restaurant, merchant). Commission rates typically range from 15% for taxis in Singapore to 20–25% for GrabFood restaurants in high-density markets such as Jakarta and Kuala Lumpur. This model keeps Grab’s marginal costs low, as the cost of each transaction is largely borne by driver-partners and merchant-partners.

2. Delivery and Service Fees

Customers pay delivery fees on food, grocery, and parcel orders. These fees vary based on distance, demand (surge pricing), and service level. Express delivery commands a premium, while subscription programmes (GrabUnlimited) offer capped or zero delivery fees in exchange for a fixed monthly fee — a powerful tool for increasing transaction frequency and reducing customer churn.

3. Financial Services Revenue

Grab Financial Group earns revenue through several streams: transaction fees on GrabPay digital wallet payments; interest income on loans disbursed through GrabFinance and the GXS/GXBank digital banks; insurance commissions from GrabInsure products; and management fees on GrabInvest products. The financial services segment is Grab’s fastest-growing revenue contributor, with total loan disbursals approaching a $3 billion annualised run rate in Q2 2025. The segment is targeting overall profitability by the second half of 2026.

4. Advertising Revenue

GrabAds monetises Grab’s data-rich, high-frequency app environment by offering brands and merchants sponsored placements, push notifications, in-app banners, and targeted offers. With 50 million monthly transacting users who provide location, purchase, and behavioural data at each interaction, Grab’s advertising platform is one of the most contextually rich in Southeast Asia.

5. Subscription Revenue

GrabUnlimited is Grab’s subscription tier, offering members reduced delivery fees, ride discounts, and exclusive promotions for a fixed monthly fee. Subscription revenue provides a predictable, recurring income stream and increases user stickiness by creating a financial incentive to consolidate all transactions on Grab rather than spreading them across competing apps.

Funding & Investors of Grab: Grab’s Journey from $10M to $40 Billion

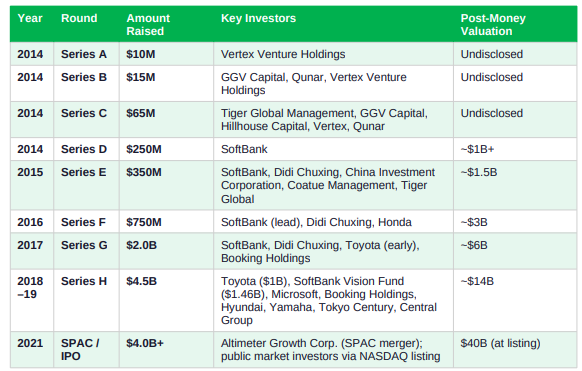

Before it became Southeast Asia’s dominant superapp, Grab had to convince some of the world’s most sophisticated investors that a Southeast Asian ride-hailing startup could become a multi-hundred-billion-dollar platform business. It succeeded — spectacularly. Over 32 funding rounds, Grab raised more than $10.4 billion in pre-IPO capital, drawing in a who’s who of global technology, automotive, travel, and sovereign wealth investors. Each funding round was not merely a financial transaction: it was a strategic partnership that gave Grab market access, technology, and credibility in a region where trust is hard to build and easy to lose.

Below is the complete timeline of Grab’s major funding rounds, from its first $10 million raise in 2014 to its landmark SPAC listing in 2021.

In December 2021, Grab completed the largest SPAC merger in history at the time, listing on NASDAQ under the ticker GRAB at a valuation of $40 billion. The deal raised over $4 billion in fresh capital, providing Grab with the runway to invest in financial services, digital banking, and AI infrastructure for the years ahead.

What the Investor Roster Tells Us About Grab’s Strategy

Grab’s investor list reads like a strategic roadmap. SoftBank’s Vision Fund — the world’s largest technology investment vehicle — provided not just capital but deep networks across Asia and strong pressure toward scale-first growth. Toyota’s $1 billion investment in Series H signalled a commitment to integrating Grab’s mobility platform with the future of automotive technology in Southeast Asia. Microsoft’s participation brought cloud computing infrastructure and enterprise credibility to Grab’s technology ambitions. Booking Holdings’ investment pointed toward travel industry integration. Didi Chuxing’s involvement (across multiple rounds) reflected mutual interests in ride-hailing dominance across Asia.

Notably, Grab attracted sovereign wealth participation through Temasek Holdings (Singapore’s state investment company), and China Investment Corporation — giving it political credibility in key markets. Vertex Venture Holdings, the venture arm of Temasek, was Grab’s very first institutional investor in Series A, a relationship that endured across multiple rounds and reflects the deep alignment between Grab’s mission and Singapore’s own ambitions as a Southeast Asian digital economy hub.

Since its NASDAQ listing, Grab has not needed to raise additional equity capital — a testament to the strength of its balance sheet and its improving cash generation. The company’s focus has shifted from fundraising to profitability, and the achievement of its first full-year net profit in 2025 marks the symbolic close of the startup chapter and the beginning of Grab’s life as a mature, self-sustaining technology business.

Financial Performance of Grab: The Road to Profitability

For much of its first decade, Grab operated at significant losses — burning cash to fund driver incentives, user promotions, and geographic expansion. This was not mismanagement; it was the deliberate cost of building network effects across eight countries simultaneously. The question the market asked from the moment of Grab’s 2021 NASDAQ listing was not whether it could grow, but whether it could grow profitably.

The 2024 results provided a clear answer. Grab reported record full-year Group Adjusted EBITDA of $313 million for 2024 — its first year of EBITDA profitability. Revenue for the year reached $2.8 billion, up 19% year-on-year. The On-Demand GMV — the total value of transactions processed across ride-hailing and deliveries — reached significant scale, demonstrating that Grab’s core business had matured.

2025 accelerated this trajectory. Grab crossed 50 million Monthly Transacting Users in Q4 2025, delivered its first full-year net profit, and achieved On-Demand GMV of $22.1 billion. Q2 2025 alone saw revenue of $819 million (up 23% YoY) and a swing from a $53 million loss to a $35 million profit — a landmark result that confirmed the business model’s unit economics had fundamentally improved.

Looking ahead, Grab’s management has set an ambitious target: to triple its profit by 2028. The company will pursue this through higher transaction volumes (driven by affordability initiatives and AI-powered service improvements), continued scaling of the high-margin financial services segment, and disciplined cost management following years of rationalisation.

Competitive Landscape: Who Challenges Grab?

Grab’s dominance in Southeast Asia is real but not unchallenged. The competitive landscape varies significantly by country, service category, and consumer segment.

Gojek / GoTo (Indonesia)

Grab’s most formidable regional competitor is Gojek, the Indonesian superapp that merged with e-commerce giant Tokopedia to form GoTo Group (listed on the Indonesia Stock Exchange). In Indonesia — both companies’ largest and most contested market — Grab holds approximately 50% of ride-hailing share versus Gojek’s 43%. Outside Indonesia, Gojek’s footprint is limited, while Grab operates across eight countries, giving it a structural scale advantage at the regional level.

Foodpanda / Delivery Hero (Food Delivery)

In food delivery, Grab’s GrabFood competes primarily with Foodpanda (owned by Germany’s Delivery Hero) in markets such as Singapore, Thailand, and the Philippines. Foodpanda has invested heavily in dark kitchens and rapid grocery delivery, but GrabFood’s advantage lies in its integration with Grab’s ride-hailing network and its broader loyalty ecosystem. In 2024, Delivery Hero sold its Foodpanda operations in several markets, a signal of competitive pressure from Grab and ShopeeFood.

ShopeeFood / Sea Group

ShopeeFood, operated by Singapore’s Sea Group (which also owns Shopee e-commerce and SeaMoney), is a growing challenger in food delivery, particularly in Vietnam where it trades market leadership with GrabFood. Sea Group’s financial strength and e-commerce integration give ShopeeFood a meaningful ecosystem advantage that makes it one of the more credible long-term challengers to Grab in the delivery segment.

Fintech Challengers (GoPay, Monee, Bank Apps)

In financial services, Grab competes with GoPay (Gojek’s digital wallet), Monee (Sea Group’s fintech arm), and a proliferating ecosystem of regional and local digital banks and fintech companies. The competitive intensity in this segment is high, but Grab’s advantage is distribution: no other fintech player in Southeast Asia can put a financial product in front of 50 million monthly active users in the context of a transaction they are already completing.

Grab’s AI Strategy: The Next Competitive Frontier

In April 2025, Grab made a significant strategic statement: it launched two AI-powered tools — an AI Merchant Assistant and an AI Driver Companion — developed in partnership with OpenAI and Anthropic. The AI Merchant Assistant helps restaurant and merchant partners optimise menu pricing, promotional timing, and inventory management. The AI Driver Companion provides real-time routing intelligence, earnings optimisation guidance, and safety alerts to Grab’s driver-partner network.

Anthony Tan has been direct about AI’s centrality to Grab’s future. In March 2025, he publicly stated that ‘humans who don’t embrace AI will be replaced by AI’ — a comment that signalled Grab’s internal culture is being actively repositioned around AI fluency. This is consistent with Grab’s broader infrastructure investment in machine learning for demand forecasting, dynamic pricing, fraud detection, and credit scoring for its digital banking products.

For Grab’s competitive position, AI is most strategically important in financial services. The ability to underwrite micro-loans and insurance products for customers with no formal credit history — using transaction data, location patterns, and behavioural signals from the Grab app — is a genuine differentiator in markets where traditional credit bureaus have thin files on large portions of the population. This data moat, built over more than a decade of daily transactions across 50 million users, is one of Grab’s most durable competitive assets.

Grab Financial Group: Banking the Underbanked

Grab’s most audacious strategic bet is its digital banking initiative. Southeast Asia has one of the world’s largest populations of unbanked and underbanked adults — estimated at over 300 million people. These individuals have mobile phones, conduct digital transactions, and earn incomes, but have historically been unable to access formal financial products because they lack credit histories, physical addresses close to bank branches, or the documentation traditional banks require.

Grab obtained digital full-bank licences in Singapore (GXS Bank, in a joint venture with Singtel) and Malaysia (GXBank, in a consortium with Kuok Group entities). Both banks launched to the public in 2023 and have grown their deposit bases rapidly. By Q4 2025, combined deposits reached $1.6 billion — and the net loan portfolio had doubled year-on-year to $1.18 billion. Loan disbursals were approaching a $3 billion annualised run rate by mid-2025, with the financial services segment targeting overall profitability by H2 2026.

The competitive advantage here is unique: Grab’s banking customers are not just banking customers. They are Grab app users with rich behavioural data — where they travel, how often they order food, whether they make consistent on-time payments for in-app services. This data allows Grab’s banks to offer credit products to customers that traditional banks would turn away, and to price them more accurately. If this model scales, Grab Financial Group has the potential to become one of Southeast Asia’s most important financial institutions.

Challenges and Risks

Despite its leading position and improving financials, Grab faces a complex set of challenges that will test its management and its model in the years ahead.

Profitability sustainability is the most immediate concern. Grab’s path from EBITDA profitability to sustainable net profit requires continued revenue growth, margin improvement in financial services, and disciplined cost management — all simultaneously. Any significant competitive intensification (for example, a well-funded new entrant or an aggressive Gojek promotional campaign) could force Grab to reinvest in incentives and promotions, pressuring margins.

Regulatory complexity across eight distinct markets is a structural challenge that has no clean solution. Ride-hailing regulations, digital banking licensing requirements, food safety rules for delivery platforms, and fintech lending laws vary enormously across the region. Grab must maintain regulatory relationships and compliance capabilities in each country — a management overhead that a single-market competitor does not face.

Driver-partner relations represent both a strength and a vulnerability. Grab’s model depends on hundreds of thousands of independent driver-partners. Rising fuel costs, changes to commission structures, or competitive pressure from other platforms can lead to supply-side disruptions that directly impact service quality and customer experience. Managing this two-sided marketplace fairly is an ongoing operational challenge.

Currency risk is an underappreciated factor for a company reporting in US dollars but earning in Indonesian rupiah, Malaysian ringgit, Thai baht, and six other currencies. Exchange rate volatility can meaningfully affect reported financial results and complicate multi-year planning.

The Road Ahead: Grab’s Outlook to 2028

Grab enters the second half of the 2020s from a position of genuine strength. Southeast Asia’s digital economy — estimated to surpass $600 billion in gross merchandise value by 2030 — is still in the early stages of its most important transition: from cash-based offline transactions to digital, platform-mediated commerce. Grab is uniquely positioned at the centre of this transition.

The company’s target to triple profits by 2028 will be driven by three growth engines: continued expansion of On-Demand GMV through affordability innovations (reaching lower-income consumers with competitive pricing), rapid scaling of the financial services segment (lending, insurance, digital banking), and AI-driven efficiency improvements that reduce the marginal cost of each transaction.

The Southeast Asian market offers additional runway that is hard to overstate. Countries like Cambodia, Myanmar, and Vietnam — where digital infrastructure is improving rapidly but Grab’s penetration relative to total addressable market remains modest — represent years of organic growth. Grab’s 129 million Annual Transacting Users, compared to a total addressable base of hundreds of millions of adults across its eight markets, shows that even the user acquisition story is far from over.

Frequently Asked Questions (FAQs)

Q: What is Grab and which countries does it operate in?

A: Grab is Southeast Asia’s leading superapp, offering ride-hailing, food and grocery delivery, parcel delivery, and financial services through a single mobile app. As of 2025, Grab operates in eight countries: Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam — serving over 800 cities and more than 50 million monthly transacting users.

Q: Who founded Grab and what is their background?

A: Grab was founded in 2012 by Anthony Tan and Tan Hooi Ling. Anthony Tan, the company’s Group CEO, is the grandson of Tan Chong Motor founder Tan Yuet Foh and holds an MBA from Harvard Business School. Tan Hooi Ling, a Cambridge graduate and former McKinsey consultant, served as Grab’s COO before transitioning to advisory roles. Both developed the initial business plan together at Harvard Business School in 2011.

Q: How did Grab become the market leader in Southeast Asian ride-hailing?

A: Grab’s dominance was built through localised strategy, aggressive funding, and a pivotal 2018 acquisition. Starting as MyTeksi in Malaysia in 2012, it expanded across the region over six years. The decisive moment came in March 2018, when Grab acquired all of Uber’s Southeast Asian operations in exchange for a 27.5% stake in Grab — inheriting Uber’s driver network, customer base, and local teams and eliminating its most powerful global competitor in one move.

Q: What is Grab’s revenue and is the company profitable?

A: Grab achieved $2.8 billion in revenue in 2024, growing 19% year-on-year, and recorded its first-ever full-year positive Group Adjusted EBITDA of $313 million. In 2025, Grab delivered its first full-year net profit — a landmark milestone — and guided for $3.33–$3.40 billion in 2025 revenue. On-Demand GMV for 2025 reached $22.1 billion, and the company crossed 50 million Monthly Transacting Users.

Q: What are Grab’s main revenue streams?

A: Grab generates revenue from five main sources: (1) commissions on ride-hailing transactions (15–25% per ride); (2) commissions and delivery fees on food, grocery, and parcel deliveries; (3) financial services income including interest on loans, transaction fees on GrabPay, and insurance commissions through GrabInsure; (4) advertising revenue through GrabAds; and (5) subscription fees through GrabUnlimited.

Q: What is Grab Financial Group and what banking products does it offer?

A: Grab Financial Group is Grab’s financial services division, offering five product lines: GrabPay (digital wallet), GrabInsure (insurance), GrabInvest (wealth management), business and consumer lending (micro-loans to driver-partners, merchants, and consumers), and digital banking through GXS Bank in Singapore and GXBank in Malaysia. By Q4 2025, the two digital banks held $1.6 billion in deposits and a net loan portfolio of $1.18 billion.

Q: Who are Grab’s main competitors in Southeast Asia?

A: Grab’s primary competitors vary by segment. In ride-hailing, Gojek (part of Indonesia’s GoTo Group) is the leading regional challenger, particularly in Indonesia. In food delivery, GrabFood competes with Foodpanda (Delivery Hero) and ShopeeFood (Sea Group). In financial services, Grab competes with GoPay, SeaMoney, and a range of local digital banks and fintech players. Despite competition, Grab is estimated to be 3–3.5 times larger than its next closest regional competitor.

Q: Is Grab publicly listed and where can I buy its stock?

A: Yes. Grab Holdings Limited listed on the NASDAQ stock exchange on December 2, 2021, under the ticker symbol GRAB, via a merger with Altimeter Growth Corp. (a SPAC). The transaction was valued at $40 billion at the time — the largest SPAC merger in history. As of May 2026, Grab’s market capitalisation is approximately $15 billion. The stock can be purchased through any brokerage with access to US-listed securities.

Q: What AI tools has Grab launched?

A: In April 2025, Grab launched two AI tools developed with OpenAI and Anthropic: the AI Merchant Assistant (which helps restaurant and merchant partners optimise pricing, inventory, and promotions) and the AI Driver Companion (which provides drivers with real-time routing optimisation, earnings guidance, and safety alerts). Grab also uses AI extensively for demand forecasting, dynamic pricing, fraud detection, and credit scoring in its digital banking operations.

Q: How does Grab’s business model differ from Uber’s?

A: While Grab started with a ride-hailing model similar to Uber’s, it diverged significantly from 2016 onward. Grab evolved into a superapp — a single platform for multiple everyday services — whereas Uber has remained primarily focused on transportation and food delivery (Uber Eats). Grab also operates digital banks and offers micro-lending products, which Uber does not. Grab’s deeper integration into the daily lives of Southeast Asian users — through payments, banking, and food — creates a switching cost that a pure ride-hailing or delivery app cannot replicate.

Conclusion

Grab’s story is one of Southeast Asia’s most compelling business narratives. In thirteen years, Anthony Tan and Tan Hooi Ling transformed a second-place Harvard Business School competition entry into a $15 billion public company that is the primary digital infrastructure for everyday life in eight countries.

The company’s 2025 milestones — first full-year net profit, 50 million monthly users, $22.1 billion in GMV — are proof that the superapp model works in Southeast Asia. More importantly, the transition from growth-at-all-costs to profitable, sustainable growth has happened without surrendering market leadership. Grab remains 3 to 3.5 times larger than its nearest regional competitor in its core markets.

The next chapter is about deepening, not widening. Grab does not need to enter new geographies — it needs to deepen financial services penetration among its existing user base, leverage AI to reduce transaction costs and improve service quality, and convert its 129 million Annual Transacting Users into more frequent, higher-value interactions. In a region of 700 million people, the addressable market is so large that even a significant improvement in wallet share among existing users would represent years of compounding growth.

For students of technology business strategy, for investors watching Southeast Asia’s digital economy, and for anyone curious about how a startup turns a local taxi problem into a continent-defining platform, Grab is essential reading. Its future is being written in every ride, every meal delivered, and every loan approved — across eight countries, in hundreds of millions of people’s daily lives.

Also Read: The Rise and Challenges of Uber: A Story of Disruption

To read more content like this, subscribe to our newsletter